WIG index volatility modelling

This project is about volatility models comparison, you can expect:

- working on the real market data (from stooq.pl)

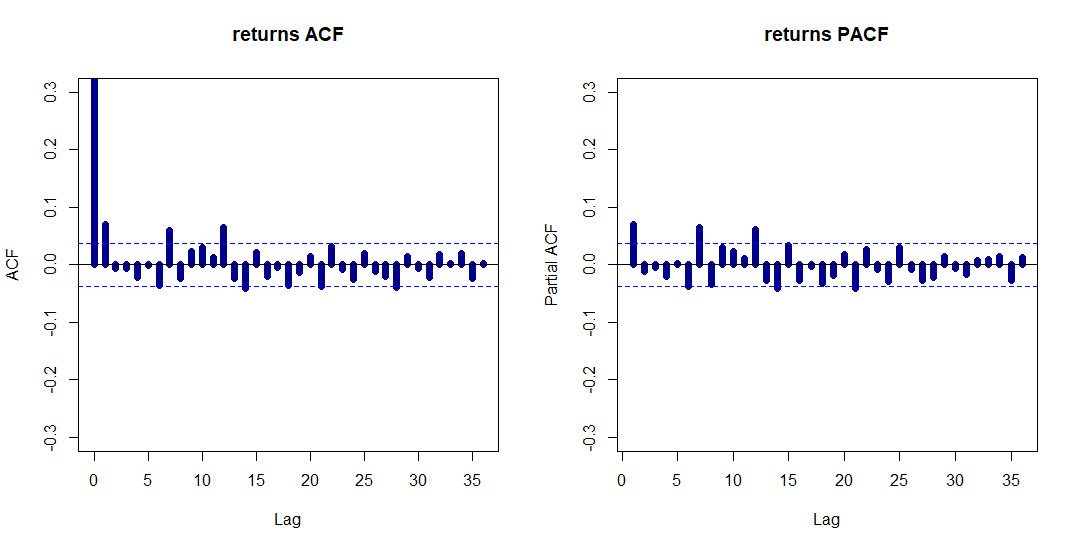

- time series data EDA (logarithmic returns transform, realization plots, ACFs, PACFs, descriptive statistics)

- statistical tests (ARCH LM, Jarque-Bera)

- GARCH modelling with prior assumptions about epsilon distribution (hypotheses)

- 4 GARCH models (standard, exponential, threshold, component) with 4 different epsilon distributions each (normal, t-student, skewed t-student, generalized error)

- 3 naive models (random walk, historical average, moving average)

- 9 performance metrics (ME, MAE, RMSE, AMAPE, TIC, MME(U), MME(O), DCP, DCPU)

- quality paper-style report in Polish